Executive Summary

The Syrian budget for 2026 is not merely a set of figures; rather, it reflects a clear attempt by the state to rebuild itself and the economy after years of conflict. It relies on a significant increase in spending aimed at improving services, supporting the economy, and launching a new phase of recovery.

However, this budget is built on a set of critical assumptions. It anticipates rapid economic growth and substantial investment, and also assumes a swift improvement in the state’s ability to collect taxes. In reality, these assumptions may be difficult to achieve in an economy still suffering from weak institutions and widespread informal activity.

On the other hand, the budget deficit is not the problem in itself, but rather how it is financed. If sufficient funding sources are unavailable, the state may be forced to resort to solutions that lead to inflation or currency depreciation, negatively affecting citizens’ purchasing power.

Furthermore, the quality of investments plays a decisive role. Not every investment leads to real growth; some investments may flow toward quick-profit sectors that do not build a productive economy over the long term.

Overall, the budget reflects great ambition to rebuild the economy, but at the same time, it depends on the simultaneous fulfillment of several difficult conditions, such as an improved institutional environment, the inflow of investments, and macroeconomic stability.

The conclusion is that this budget is an economic gamble: if these conditions are met, it may help launch recovery; if they are not, it may lead to new economic pressures instead of solving existing problems.

Introduction

The importance of addressing Syria’s 2026 budget stems from the fact that it does not merely represent a document for a single fiscal year. Rather, it represents a revealing moment regarding the nature of the ongoing transformation in the state’s perception of its economic function and the limits of its ability to use fiscal policy as a tool to simultaneously rebuild legitimacy, institutions, and economic activity. In post-conflict economies especially, the general budget is not a purely accounting matter; it becomes a dense political and economic text that encapsulates a vision of the state, the market, and society, revealing actual priorities more than public rhetoric does. For this very reason, reading this budget gains importance that goes beyond analyzing expenditure and revenue items, extending to an assessment of the nature of the proposed economic model, the limits of its feasibility, and the relationship between its political ambition and its macroeconomic and institutional constraints.

This article proceeds from the fundamental premise that understanding the 2026 budget cannot be achieved through a fragmented numerical reading or a descriptive approach that merely presents indicators. Rather, it requires deconstructing the budget’s internal structure and linking it to three interconnected circles: First, the direct fiscal significance of the budget as a tool for the state’s financial, security, service, and investment repositioning; second, the relationship between fiscal policy and monetary policy, including the question of the deficit, price stability, and the limits of coordination between fiscal expansion and monetary discipline; and third, the macroeconomic constraints imposed by growth requirements, the volume of investment needed, the economy’s absorptive capacity, and the characteristics of the institutional environment in a post-conflict state.

These circles do not function as separate levels of analysis but as an interconnected system, where a flaw in one—whether in the revenue structure, financing conditions, or institutional capacity—transfers directly to the other levels and reshapes their outcomes.

Accordingly, the article progresses from reading the budget itself and its direct implications, to analyzing its fiscal and monetary philosophy, and then to testing it within the structural constraints of the macroeconomy and institutional political economy. The purpose of this sequence is not only to organize the discussion, but to demonstrate that the central problem in such budgets lies not in a single figure or an isolated item, but in the degree of consistency between declared objectives, available tools, and the constraints governing actual economic reality.

In this sense, the article does not seek to evaluate the budget solely based on its size or items, but based on its internal logic: that is, its ability to combine expanding the state’s role, maintaining monetary balance, and building a productive and institutional base capable of supporting this expansion.

The Significance of the Budget and the Repositioning of the State

If we look at Syria’s 2026 budget, it does not appear as a mere annual financial statement, but as a document that reveals, with considerable clarity, the new administration’s vision of the nature of the upcoming economic phase, the state’s position within it, and the tools it believes capable of launching recovery. The first thing to be said, before delving into any theoretical or technical detail, is that this budget says something specific and direct: the state believes that 2026 is not an ordinary year, but a foundational one, and that it must act financially on a scale and at a speed far exceeding the logic of traditional public administration, which is typically based on limiting spending within the bounds of existing revenues, avoiding large deficits, and adopting gradualism in fiscal expansion, prioritizing stability over using the budget as an active tool to reshape the economy or accelerate growth.

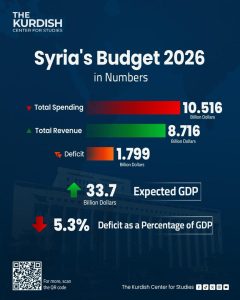

The estimated expenditure volume reaches $10.516 billion, against expected revenues of $8.716 billion, with a deficit of $1.799 billion, equivalent to 5.3% of the expected gross domestic product of $33.7 billion. The document also shows that 2025 witnessed revenues of approximately $3.447 billion and expenditures of approximately $3.493 billion, with a slight surplus or saving according to the official presentation. It confirms that the 2026 budget increases to more than three times the levels of previous years, reflecting a clear transition from the logic of management and preservation to the logic of expansion and reshaping the state’s economic role.

The primary significance of these figures is not merely that the state has expanded its spending, but that it has redefined itself financially. The transition from a spending volume of nearly $3.5 billion to over $10.5 billion within a single cycle cannot be understood as a gradual correction, but as a state leap—a sovereign decision to reassert the state’s financial, security, service, and investment presence all at once. Hence, this budget, in its essence, is not a budget of continuity, but a budget of state repositioning.

However, a careful reading of the budget reveals an important internal tension from the outset. The document uses cautious language regarding the deficit, emphasizes fiscal sustainability, avoiding deficit financing, and aligning spending growth with available resources; it even celebrates achieving a limited surplus in 2025 as an indicator of “rational financial management.” At the same time, the 2026 budget adopts a relatively large deficit, embraces broad fiscal expansion, and builds its vision on a very large increase in spending and on the assumption of a strong acceleration in economic activity. Here, we are not merely facing a difference between one year and another, but a contradiction between the rhetoric of discipline and the practice of expansion. This is not a rhetorical detail, but a fundamental analytical point: because the budget, in this sense, announces the transition from the logic of “correcting public finances” to the logic of “using public finances as a tool to rebuild the economy and the state,” without sufficiently declaring this transition theoretically.

This meaning is confirmed if we look at the spending structure. The budget allocates 60% of spending to current expenditures, 27% to investment expenditures, and 13% to subsidies and social security. At the sectoral level, 41% of expenditures go to defense and national security, 33% to health, education, and social protection, and 26% to public services. These figures clearly state that the state does not begin with production, but with re-establishing sovereignty and administration. Security first, then restarting the government apparatus, then social and service spending, and finally investment as a tool for launching recovery.

From a public finance perspective, this arrangement is understandable in a post-conflict state. High security spending is not merely a political choice, but a reflection of the state’s desire to restore its monopoly on legitimate force and unify the public space. Similarly, the rise in current expenditures is not necessarily a sign of failure, as it largely reflects the restarting of institutions, salaries, administration, maintenance, and basic services.

However, the fact that this expansion is understandable in terms of its motives does not necessarily mean it is sustainable in terms of its conditions. The difference between necessary expansion and excessive expansion is determined not by intentions, but by the economy’s and institutions’ ability to absorb this expansion without generating macroeconomic imbalances.

In this sense, the reading of this expansion cannot be separated from two questions that will appear later in the analysis: first, the realism of the assumptions underlying the revenues intended to finance it; and second, the ability of the monetary system to absorb this expansion without turning into inflationary pressures or an exchange rate imbalance.

From a macroeconomic and developmental perspective, however, this arrangement carries a clear paradox: the state says it wants to launch growth, yet it allocates the largest share of its direct spending to stabilizing the political and administrative system before building a sustainable productive base. This means the budget carries an institutional-sovereign logic more than a purely productive one.

Revenues and Their Structural Implications

If spending reflects the state’s will to reposition itself, revenues reveal the limits of that will. The budget relies on a mix of taxes and fees, oil revenues, and other returns, including state investments. According to budget estimates, out of total revenues of $8.716 billion, tax revenues and fees constitute the largest portion at approximately $5 to $5.5 billion, followed by oil revenues in the range of $1.5 to $2 billion, and then the “other revenues” item, which approaches $1.5 to $2 billion, including returns from state investments and various other sources.

This distribution gives an initial impression of diversity, but it hides a fragile and unstable revenue structure. Taxes, especially in a post-conflict economy, do not only reflect financial decisions; they reflect administrative and institutional capacity. Achieving approximately $5 billion in tax revenue implicitly assumes the existence of an effective collection apparatus, the ability to control evasion, and a relatively organized economic environment. These are conditions that have not yet fully materialized, making this largest portion of revenues contingent on rapid improvement in public administration.

The impact of this institutional constraint is not limited to the revenue side alone but extends to the structure of the economy as a whole. The expansion of the informal economy and weak tax compliance not only reflect limited collection, but also point to an unstable and unpredictable business environment—factors that directly limit the economy’s ability to attract long-term productive investment.

As for oil revenues, estimated at $1.5 to $2 billion, despite their importance, they are inherently highly volatile and depend on political, security, and technical factors beyond the state’s full control, such as production stability, global energy prices, and export capacity. Consequently, relying on them, even at this volume, adds an element of structural uncertainty.

The most sensitive item remains what is called “returns from state investments,” which falls under the “other revenues” category valued at nearly $1.5 to $2 billion. This item, despite its notable relative size, lacks sufficient detail to clarify its nature: does it arise from genuine operating profits from state-owned assets, from asset restructuring, or from exceptional or non-recurring revenues? This ambiguity not only reduces the budget’s transparency but also weakens the ability to assess the sustainability of these revenues.

Furthermore, this revenue structure raises an additional question regarding the nature of the economic model itself: the high share of non-tax revenues, even if it does not reach the levels of classic rentier economies, may indicate a partial reliance on income sources not directly linked to broad productive activity. In this case, the challenge is not only in the volume of revenues but in their type—whether they reflect a productive economy expanding horizontally through the tax base, or an economy tending toward the reproduction of various forms of rent, whether through assets, privileges, or low-value-added activities.

This structure also points to an important normative issue regarding the ratio of tax revenue to GDP. By a simple calculation, the estimated tax revenues between $5 and $5.5 billion represent approximately 14% to 16% of the $33.7 billion GDP. This percentage falls at the lower limit of what the economic literature considers necessary to build a fiscally capable state, where a level of 15% is usually cited as a threshold for fiscal sustainability. However, the more appropriate comparison in this case is not with global averages, but with post-conflict or fragile states, where this ratio typically ranges between 5% and 10% in the early stages of recovery, and may gradually rise to only 10% to 15% after years of institutional rebuilding.

Therefore, reaching this percentage at this stage does not necessarily reflect achieved tax capacity, but rather an implicit assumption of a rapid leap in institutional efficiency and a broadening of the tax base—an assumption that carries a high degree of uncertainty.

Thus, this percentage transforms from an accounting indicator into a highly sensitive structural indicator: on one hand, it reflects an ambition to reach the threshold of a fiscally viable state; on the other, it reveals that achieving this ambition assumes institutional conditions that have not yet taken root.

The significance of this assumption is not limited to fiscal balance; it also extends to the logic of growth itself, as the same institutional conditions necessary for expanding the tax base are those required to attract productive investment. This means that any weakness in fulfilling these conditions will be reflected simultaneously in revenues and in the growth path assumed in the budget.

Therefore, although total revenues amount to $8.716 billion, their composition reveals that a significant portion depends on institutional and economic assumptions that have not yet been fully established. Based on this, it can be said that the problem with revenues is not in their nominal volume, but in their institutional quality. They are possible revenues, but not guaranteed. This means any deviation in the assumptions associated with them will directly affect the deficit and fiscal balance.

Fiscal Policy and the Limits of Monetary Balance

Here we enter the second issue: fiscal policy itself. What is the fiscal philosophy of this budget? The answer: it is an expansionary budget, even if wrapped in cautious rhetoric. It does not merely increase appropriations; it adopts a vision that government spending, alongside improved confidence and the return of activity, can be a lever for a broad economic takeoff. However, fiscal expansion in itself is not a criterion for judgment; it may be a necessary expansion in a reconstruction phase. The real criterion is: How is it financed? What is its impact on monetary balance? And how consistent is it with the supply side of the economy?

In this specific context, the question of financing cannot be separated from the revenue structure analyzed previously. The fragility of the revenue base means that any deviation in collection will translate directly into financing pressures, making the relationship between public finances and monetary policy a structural relationship, not merely technical coordination.

This leads us to the relationship between fiscal and monetary policy—the decisive relationship without which the budget cannot be read. The document speaks of a commitment to avoid deficit financing, to price stability, to enhancing confidence in the lira and the banking system, to the return of deposits, and to reducing reliance on cash outside the financial system. At a theoretical level, this is a necessary condition: if fiscal policy expands without controlling financing, monetary policy becomes a subordinate tool and price stability is undermined. If monetary policy tightens more than necessary in a weak economy, it may stifle recovery. Consequently, the success of this budget assumes precise coordination between calculated fiscal expansion and a monetary system capable of absorbing shocks.

But this condition is insufficient. Even in the absence of direct monetary financing, inflationary pressures can arise from an imbalance between demand and supply. The budget itself builds on a leap in aggregate demand: the return of residents, improved remittances, expanded consumption, and increased investment. If demand precedes the recovery of supply—constrained by infrastructure, productive capacity, supply chains, and institutions—what might be called “deferred inflation” appears: inflation that does not arise from direct monetary expansion, but from a time gap between the acceleration of demand and the slowness of supply response.

However, the issue does not stop at demand-driven inflation; it intersects directly with the nature of investment itself. Part of the expected investment flows may turn in the short term into consumer demand or fast-turnover activities, instead of becoming sustainable productive capacity, thereby deepening the gap between demand and supply and increasing inflationary pressures.

The risks associated with the deficit are not limited to this indirect channel; they extend to how it is financed in the context of an economy with limited financing options. While the budget emphasizes avoiding deficit financing, this commitment remains subject to testing if revenue or investment assumptions are not realized. In a post-conflict economy, where local debt markets are narrow and access to external financing is restricted, monetary financing becomes an implicit option even if not declared.

The danger here lies not only in the direct printing of currency, but also in the seductive nature of this option when public finances face immediate pressures, and in the weakness of institutional constraints that might prevent its use. Moreover, large fiscal expansion in a fragile banking environment may reflect as indirect monetary expansion through banking channels, putting pressure on the exchange rate and fueling inflation.

In this context, the exchange rate constitutes the most sensitive channel for the transmission of these imbalances. Any direct or indirect monetary expansion associated with deficit financing may quickly translate into pressure on the currency, transforming fiscal imbalance into imported inflation and undermining a large part of the real impact of public spending on purchasing power.

Consequently, the relationship between the deficit and monetary stability in this case is governed not by declared intentions, but by the ability of the financial and institutional system to resist sliding toward inflationary financing, whether directly through monetary issuance or indirectly through credit expansion linked to public spending.

In this sense, the monetary challenge is not separate from the other elements of the budget; it represents a meeting point between weak revenues, the nature of spending, and the expected growth pattern, making any flaw in one of these components rapidly transferable to monetary stability.

Macroeconomic Constraints and the Assumed Growth Logic

From here, we enter the macroeconomic constraints. The budget anticipates real economic growth of between 8% and 10%, and even suggests in some places that it may exceed 10%. It links this growth to several factors: the end of structural constraints, improved economic management, the return of oil and gas fields, the return of Syrians, increased spending on services, improved energy, increased investment in construction, transport, energy, and tourism, and improved remittances from abroad. In principle, it is not impossible for economies emerging from rock bottom to achieve high growth rates. But macroeconomic analysis asks not only whether growth is mathematically possible, but: What are the requirements for this growth? Does the budget finance them? And can the economy absorb them?

If we take the expected GDP at $33.7 billion, 10% growth means adding production of nearly $3.3 billion in one year. If we apply the logic of the Incremental Capital-Output Ratio (ICOR) in its typical range for developing and transitional economies—between 3 and 8—achieving growth of this magnitude requires investments ranging roughly between $9 and $24 billion, with an average approaching $17 billion. This is not merely a calculation; it is a tool to reveal the internal tension in the budget: because government investment spending does not exceed about 27% of $10.516 billion, i.e., approximately $2.8 billion only. This means the bulk of the investment needed to achieve the target growth must come from the private sector or abroad. In other words, the budget does not create growth from within; it assumes that the economy and the political and financial environment will generate it around itself.

However, this analysis implicitly assumes that the expected growth results from new investments, whereas a significant part of growth in post-conflict economies may result from what is known as rebound growth—the restarting of productive capacities that were idle due to improved security conditions and the return of economic activity. In this case, part of the growth can be achieved without the need for large investment flows, meaning that short-term growth may not reflect a structural improvement in productive capacity.

Nevertheless, this type of growth is naturally temporary, as it recedes once idle capacities are exhausted, at which point the real constraint appears: the need for new productive investments. This may reveal a gap between realized growth and sustainable growth.

Here, this hypothesis intersects directly with what was previously raised regarding institutional constraints: the same environment facing difficulties in expanding the tax base is the one that may limit the economy’s ability to attract broad productive investments, making this scenario dependent on simultaneous institutional improvement at multiple levels.

Moreover, the existence of a rebound component in growth may lead to inflated revenue expectations in the short term, where realized growth might be interpreted as evidence of permanent economic expansion, whereas it may partly reflect the recovery of previous activity—increasing the risk that expected revenues will not materialize in the medium term.

Here, the issue becomes even clearer: the budget is not only optimistic, but built on a central external assumption. It assumes that large flows of private, local, and foreign investment will enter the economy in a short period, that they will flow into productive sectors sufficient to raise real output quickly, and that the institutional and security environment will allow for this. This is a very strong assumption. In post-conflict economies, it is not enough to lift restrictions or announce openness for deep productive investment to flow. Typically, quick capital, real estate, trade, and short-cycle service activities enter first, while long-term productive investment requires a much higher degree of legal, institutional, and political certainty.

Consequently, the problem concerns not only the volume of expected investment but also its nature: investment flows in such environments may tend toward rentier or semi-rentier sectors that yield quick returns but do not build a sustainable productive base. This means part of the achieved growth may be formal or short-term growth, rather than deep productive growth.

But even if we assume these flows will arrive, we encounter the next constraint: absorptive capacity. An economy of $33.7 billion cannot usually absorb investments at any level and any speed without bottlenecks. If we use the estimate we discussed—based on the premise that the maximum absorptive capacity of an economy in post-conflict conditions may not exceed, at best, about 50% of GDP, an estimate linked to factors such as institutional efficiency, infrastructure readiness, labor market flexibility, and the administrative apparatus’s ability to implement projects—this aligns with estimates in the literature on transitional economies. Accordingly, the Syrian economy might be able to absorb between approximately $15 and $17 billion. This figure, as is clear, lies very close to the average investment required to achieve 10% growth.

However, this apparent proximity hides a high degree of fragility. It means the economy is assumed to operate near its maximum capacity, leaving very little margin for error or deviation.

This margin narrows further if we consider that part of the growth may be rebound in nature, meaning the real investment component of growth may be less than what the aggregate figures suggest, increasing the economy’s sensitivity to any slowdown in new investment flows.

This implies that the budget builds its optimistic scenario on the assumption that the economy will operate near its maximum limits of absorption. This narrows the margin of error to the minimum. If investments come in lower, growth declines and revenue collection falters. If they come in higher than the economy’s capacity, the excess turns into inflation, rising asset prices, bottlenecks, and misallocation.

In light of what was presented in the monetary section, this scenario is not limited to growth risks alone but extends to monetary stability, as unbalanced investment flows may turn into additional demand pressures instead of turning into supply, deepening the imbalance between the two sides.

From a macroeconomic perspective, this is the most important point in evaluating the budget: the danger is not only in the size of the deficit, nor only in the optimism of growth, but in the fact that the relationship between required growth, necessary investment, and available absorptive capacity is stretched to the maximum. We are facing what can be called the “equation of absolute success”: massive investments must come, but not exceed the economy’s absorptive capacity; they must go to productive sectors, not to speculation; they must turn quickly into real growth, not just price increases; and they must result in improved revenues before the deficit puts pressure on balances. This is a theoretically possible equation, but a practically rare one.

Institutional Political Economy: The Market, Rent, and the State

At this precise point, considerations of institutional political economy intersect. The budget cannot be read only as macroeconomic figures, but as a document attempting to rearrange the relationship between the state, the private sector, and society. It presents the private sector as a “fundamental partner” in development, emphasizes encouraging investment, expanding investment opportunities, improving the business environment, addressing non-performing loans, and enhancing the role of telecommunications, digital transformation, and infrastructure—even limiting the public sector’s crowding out of the private sector. From a theoretical direction, this is an important shift, and can even be considered one of the budget’s strengths, as it implicitly recognizes that the state alone is unable to finance reconstruction and create growth.

But in political economy, it is not enough to refer to the “private sector” in an abstract formula. The decisive question is not: Will the private sector be empowered? But rather: Which private sector? Is it a productive, competitive, long-term private sector that enters manufacturing, exportable services, and infrastructure? Or is it a rentier private sector, close to the authorities, capturing privileges, assets, contracts, and real estate opportunities? In transitional economies, especially those emerging from conflicts, this difference is vital. Because “empowering the private sector” may indeed mean building a productive market economy, or it may mean recycling rent in a new form.

In this sense, what was previously raised regarding the revenue structure and the nature of expected investment finds its extension here. The form of revenues is not separate from the form of the economy itself, nor is the pattern of investment separate from the institutional structure that guides it. An economy partially reliant on non-tax revenues of unclear source, and expecting rapid investment flows, is prone to heading toward forms of rent even without explicitly declaring so.

Hence, one of the most important areas of institutional ambiguity in the budget is that it proposes partnership with the private sector as a solution, but it does not sufficiently deconstruct the institutional framework that will prevent this partnership from turning into a new rentier alliance between the state and capital.

This means the central question concerns not only the size of the private sector’s role, but the nature of the relationship that will emerge between it and the state: will it be a relationship of competition and production, or a relationship of privileges and redistribution of resources?

The same applies to the social dimension of the budget. It clearly declares that it targets improving wages, combating poverty, expanding social protection, improving health and education, launching the “Syria without Camps” plan, developing affected areas and the Jazira region, and rehabilitating the service infrastructure. In terms of political and social intent, this is important and positive, indeed necessary for rebuilding legitimacy. But from a public economics perspective, a distinction must be made between declaring a social goal and the ability to actually achieve it. Increasing wages in a transitional environment may mean real improvement if accompanied by price stability and increased productivity, but it may turn into mere nominal compensation if consumed by inflation. Poverty reduction plans require data, targeting, and implementation mechanisms, not just general appropriations. Ending camps requires massive urban, financial, and institutional capacity, not just political direction.

Furthermore, the effectiveness of these social policies is directly linked to what was analyzed previously at the monetary level; any imbalance in price stability or the exchange rate may undermine a large part of their real impact, making their success conditional on a macroeconomic stability that the budget does not fully guarantee.

Consequently, the budget scores a positive point regarding the clarity of social intent, but it remains much weaker in terms of the executive engineering necessary to transform this social intent into measurable results.

Here, the core of the institutional problem emerges. The budget itself admits that delays in reforms and capacity building within institutions may delay results. It also acknowledges geopolitical risks, inflation risks, and external factors that may raise costs or delay some projects. This is an important admission.

But this admission leads to a more profound conclusion: the fundamental gap is not merely a resource gap, but an implementation capacity gap. The planned spending volume requires an administrative and institutional apparatus capable of contracting, implementation, oversight, and evaluation—conditions that are not usually fully present in the early stages of recovery.

In this case, the danger is not only in failing to achieve objectives, but in the fiscal expansion itself becoming a source for reproducing new imbalances, whether through resource misallocation, the strengthening of influence networks, or the direction of investment toward sectors with quick political returns instead of sustainable economic returns.

In post-conflict states, the decisive problem often lies not in formulating a vision, but in the state’s capacity for contracting, procurement, follow-up, oversight, coordination, pricing, and directing investment. The higher the volume of investment and expansionary spending in a fragile institutional environment, the greater the risk of shifting from “developmental expansion” to “unimplemented expansion” or “low-efficiency expansion.”

Thus, this section not only constitutes an extension of the previous analysis but provides an explanation for it: many of the risks that appeared in revenues, monetary balance, and the logic of growth find their roots in this institutional structure, making it the real pivot for evaluating the budget.

Conclusion

If we gather all the above, the picture of the budget becomes clear in a more precise form. On one hand, it has real positives that should not be overlooked. It presents a clear vision for reconstruction, recognizes the importance of the private sector, allocates a non-negligible investment percentage, gives the social aspect a significant place, shows awareness of some macroeconomic risks, and attempts rhetorically to link fiscal expansion with maintaining monetary stability. All of this makes it better than formal or closed budgets that see nothing but narrow accounting.

On the other hand, it has clear structural negatives: the contradiction between the language of fiscal caution and the practice of expansion; reliance on revenue sources that assume rapid institutional improvement, including achieving a relatively high level of tax revenue compared to the reality of a post-conflict economy; excessive optimism regarding growth and investment; lack of detail in some revenue items, especially returns from state investments; the large weight of security spending; and an implicit reliance on market forces and external financing to bridge the gap between ambition and government funding.

As for the risks, they are central, not marginal. First, private and external investments may not come in the assumed volume or speed, leading to lower growth, lower revenues, and a larger deficit. Second, if investments do come, they may go to rentier or real estate sectors that do not generate sufficient productive growth. Third, the constraint of absorptive capacity may turn large flows into inflation, rising asset prices, and implementation bottlenecks. Fourth, the expansion in demand, driven by spending, remittances, and returning residents, may precede supply recovery, putting pressure on prices and the exchange rate even without direct monetary financing of the deficit. Fifth, weak institutional capacity, including tax capacity, may make a significant portion of investment spending and social programs much less effective than the document assumes.

When these risks are viewed in light of the analyzed interconnectedness between revenues, financing, investment patterns, and institutional structure, they do not appear as independent risks, but as different expressions of a single common constraint: the limited institutional capacity to transform fiscal expansion into sustainable growth without generating macroeconomic imbalances.

The conclusion forced by this analysis is not that the budget is “bad” or “impossible,” nor is it a reassuring or conservative budget. It is, more accurately, a high-ambition transitional budget with a narrow margin of safety. Its primary strength is the clarity of direction: rebuilding the state, restarting the economy, empowering the private sector, and expanding the state’s social presence. Its primary weakness is that it links its success to a long chain of simultaneous conditions: security stability, institutional improvement, investment flow, improved energy, rapid growth, a real rise in the state’s tax capacity, monetary stability, and a recovery in confidence. In economics, the more conditions that must be met together, the weaker the reliability of the baseline scenario.

In this sense, the real challenge revealed by this budget lies not only in achieving these conditions, but in achieving them simultaneously, which makes it akin to a delicately balanced equation, where the imbalance of any element may lead to a rapid transfer of imbalances across the rest of the economy.

Therefore, a dispassionate evaluation of this budget must say clearly: it is not a budget of sustainability in the strict sense, but a budget of a gamble. A gamble that the state can expand fiscally without losing monetary control; that the economy can grow rapidly without hitting its absorptive constraints; that the private sector and foreign investment will turn into a productive force rather than a new recycling of rent; and that state institutions, including its tax apparatus, are capable of translating appropriations into results. These are gambles that are not impossible, but they are very large.

Unless these conditions are met, the budget may transform from a tool for reconstruction into a new source of imbalance, not because of its goals, but because of the gap between its ambition and the institutional capacity to implement it.

For this very reason, what 2026 will reveal is not only the accuracy of financial estimates, but the extent of the new Syrian state’s ability to solve the classic knot of every post-conflict economy: how to expand the state without destabilizing the macroeconomic balance, how to unleash the market without reproducing rent, how to build real tax capacity, and how to announce recovery before its institutional tools have fully matured.

{kind=link}